Segment Wealth Musings

Smart Money? Maybe. Brilliant Money? Never.

Like all industries, there is a pecking order in the investment arena, a hierarchy, if you will. At the top of the financial pyramid are the hedge fund and private equity businesses. At the base of the pyramid is the bank teller. While often grouped together, the hedge fund and private equity businesses are very different since hedge funds normally trade in listed securities that are available to everyone. In contrast, private equity is comprised of companies that don’t trade anywhere. Those listed securities in the hedge fund space could be options, stocks, preferreds, bonds, futures, and may or may not include leverage, or borrowed money.

While my personal experience is anecdotal, I feel it represents the results experienced by most. My personal investments in hedge funds have always turned out poorly, and my private equity experience has generally turned out favorable. I learn my lessons the hard way, like everyone else.

Hedge funds are often marketed exclusively to the rich because, as private-placement vehicles, they have a “qualified purchaser” requirement (normally meaning a $5 million investor net worth requirement). This exclusivity has the ego effect of making hedge funds sexy, while the truth is that this feature is a regulatory mandate. Hedge funds have a unique traditional compensation arrangement, referred to as “2&20.” The “2” represents the 2% annual management fee, and the “20” is the manager’s 20% of retained profit split as a performance fee.

A study called “The Performance of Hedge Fund Performance Fees” released on June 23, 2020, put specific data to the indigestion hedge funds have caused me over the years. It seems I have lots of company in my minor misery.

The study was completed by a trio of researchers from Ohio State University and the University of Arizona. I won’t bore you with the totality of its 61 pages of findings, so a summary will have to suffice, and you can read more by clicking here.

The study was an exhaustive look at the relationship of gross fund returns to net (after fees) fund returns. It studied the entire universe of funds in aggregate, thus addressing “survivorship bias,” which allows the performance of dead funds to be swept under the rug, leaving only surviving funds to tell their story. Because the study looked at 100% of registered funds in each of 22 sequential years, it solves the problem of natural, but sometimes deliberate, selective sampling so prevalent when drawing comparisons.

The data for the study were provided by BarclayHedge and Lipper. The study period started in 1995, the year that both data providers began keeping a graveyard file of dead fund data.

With 22 years of data (1995-2016), an aggregate view of the hedge fund industry’s results is enlightening. A large number of new funds proliferated until the 2008 market crash sent the industry reeling, and since then, funds have died off in greater numbers than new entrants. The industry comprised just 80 funds in 1995, peaked at 2,156 funds in 2008, and finished the study period in 2016 with just 1,490 registered funds. Another interesting snippet is that a total of 5,917 funds existed during the study period, with 4,700 ending up in the so-called “graveyard,” highlighting the importance of avoiding survivorship bias. Only 21% of funds surviving is an interesting data point on its own.

Considering that hedge fund managers are purported to be the smartest of the smart, the returns were worse than I surmised. The industry’s annualized aggregate gross results posted over the time period were 5.8% before fees and just 1.9% after fees. This is painfully behind the 9.55% earned by the S&P 500 in the same time period, which is available in the marketplace at near-zero cost. The study did not report on taxes on the 1.9% returns, but considering the nature of hedge fund activity, it’s safe to assume some negative tax implications hindered returns further.

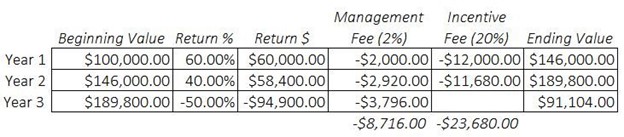

The most amazing set of stats in the report concerned the effect of the incentive fees’ asymmetric nature. Because of the lumpy nature of returns, profit incentive fees were often charged even when losses prevailed. You can see in the example below, that after year 3 the fund has a net loss, while the fees charged during the life of the fund total more than 30% of the original value.

Because the funds don’t return prior paid fees when results lag, many unintended consequences result. Many funds will simply close up shop if they get too far underwater, or the fund manager might adopt more aggressive strategies since they may have less skin in the game at that point. This contributes greatly to the 79% fatality rate, but it gets worse.

For the first 13 years of the study, those lumpy returns, coupled with an awful market in 2008, conspired to generate -$1.3 billion in aggregate overall fund losses, while still generating nearly $52 billion in fees for the incentive component alone in the same time period. That number does not include management fees. While the vast majority of funds had a 20% incentive fee listed in their client agreement, the average was 18.97% since some fees were lower in the study. However, the actual incentive fees charged were not 18.97% but were actually over 45% due to the asymmetric nature of the incentive agreement. The study did not conclude that anyone was treated unfairly or that the fees were calculated incorrectly. That’s just how the math worked out when the dust settled from all the peaks and valleys and passage of time.

By the end of the study period in 2016, the industry did manage to eke out an overall profit for investors, albeit a small one. The industry earned an incredible profit for itself, however. One would assume that the $228 billion earned in profits would have generated incentive fees of 18.97%, or $43.3 billion. Yet, the asymmetry of returns caused the actual earned fee to be $113 billion, or about $70 billion higher than the agreed fee, while still being technically correct.

This study makes it pretty clear to me that my intuition is well-founded. I have no doubt that smart investors are running hedge funds, and maybe they’re smarter at running a business than they are at investing. I simply question how smart it is to engage them.

Please See Important Disclosure Information.